When you sell investments for a profit, you owe capital gains tax. But how much you pay depends significantly on how long you held the investment. Understanding the difference between short-term and long-term capital gains—and how to minimize taxes legally—can save you thousands.

Capital Gains Tax Rates (2026)

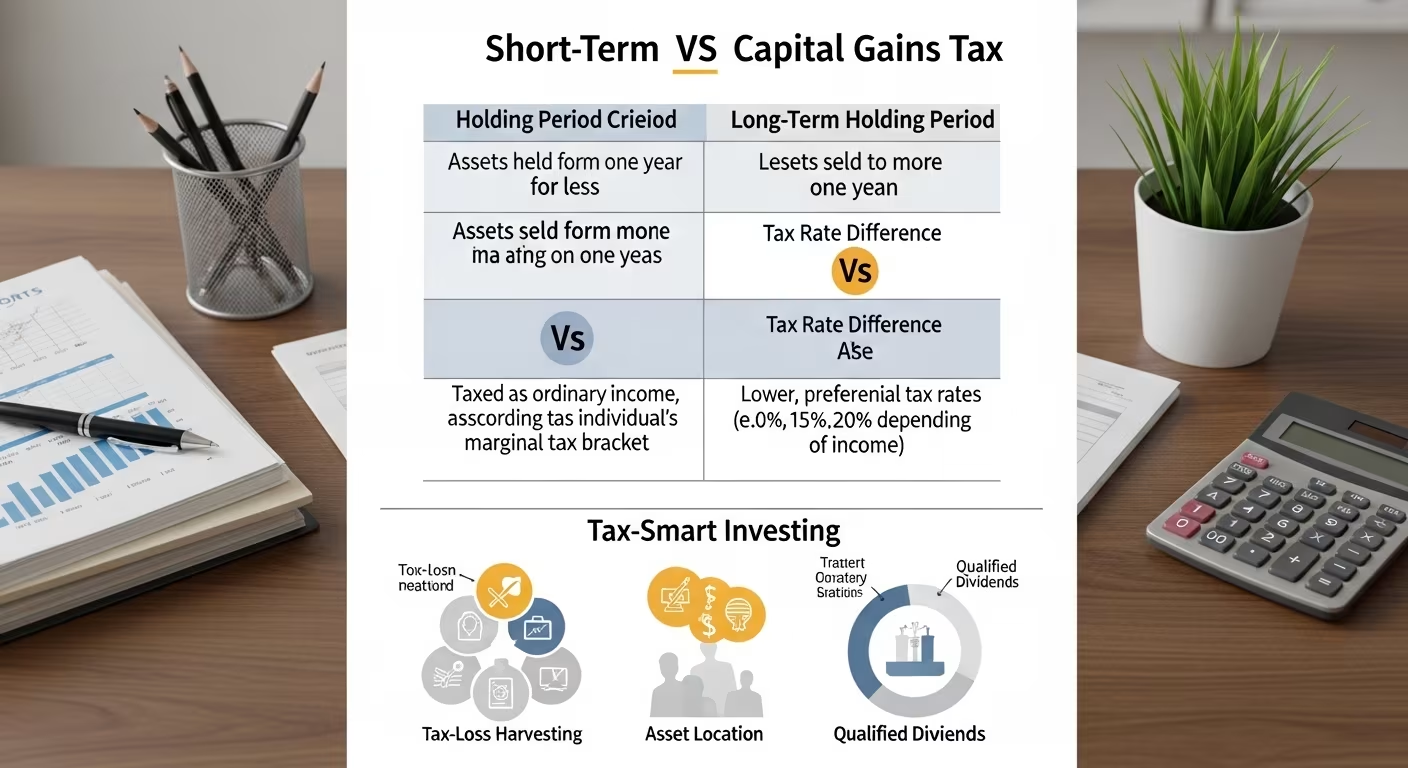

Short-Term Capital Gains (Assets Held Less Than 1 Year) Taxed as ordinary income at your marginal tax rate (10-37%).

Long-Term Capital Gains (Assets Held 1+ Years)

| Taxable Income (Single) | Tax Rate |

|---|---|

| $0 - $48,350 | 0% |

| $48,351 - $533,400 | 15% |

| $533,401+ | 20% |

Plus: Net Investment Income Tax (NIIT) of 3.8% on investment income for singles earning over $200,000 and couples over $250,000.

The Difference in Dollars

| Scenario | Short-Term (22% bracket) | Long-Term (15%) | Tax Savings |

|---|---|---|---|

| $5,000 gain | $1,100 tax | $750 tax | $350 saved |

| $10,000 gain | $2,200 tax | $1,500 tax | $700 saved |

| $50,000 gain | $11,000 tax | $7,500 tax | $3,500 saved |

| $100,000 gain | $22,000 tax | $15,000 tax | $7,000 saved |

The lesson: Holding investments for at least 366 days before selling can save you 7-22% on taxes. For a $100,000 gain, that is $7,000-22,000 in tax savings—just for waiting one extra day.

Tax-Loss Harvesting: Offset Your Gains

Sell losing investments to offset capital gains dollar-for-dollar. If you have $10,000 in gains and $7,000 in losses, you only pay tax on $3,000. Plus, you can deduct up to $3,000 in excess losses against ordinary income each year, carrying forward any remaining losses indefinitely.

Watch rule: You cannot buy back the "substantially identical" security within 30 days before or after selling at a loss (wash sale rule). Buy a similar but not identical fund (e.g., sell VTI, buy ITOT).

What Is Capital Gains Tax?

The Basic Concept

Capital gain = Selling price - Purchase price (cost basis)

Example:

- Bought stock for $5,000

- Sold for $8,000

- Capital gain: $3,000

You owe tax on that $3,000 gain.

Types of Capital Assets

Capital gains tax applies to:

- Stocks and bonds

- Mutual funds and ETFs

- Real estate (with exceptions)

- Cryptocurrency

- Collectibles

- Business interests

- Personal property (vehicles, jewelry)

Cost Basis

Your cost basis includes:

- Original purchase price

- Transaction fees (commissions)

- Reinvested dividends (for funds)

- Improvements (for real estate)

Higher basis = lower gain = less tax

Short-Term vs. Long-Term: The Critical Difference

Short-Term Capital Gains

Holding period: One year or less

Tax rate: Your ordinary income tax rate (10%-37%)

Example: 24% tax bracket + $10,000 short-term gain = $2,400 tax

Long-Term Capital Gains

Holding period: More than one year

Tax rate: Special preferential rates (0%, 15%, or 20%)

Example: $10,000 long-term gain at 15% rate = $1,500 tax

2026 Long-Term Capital Gains Rates

| Taxable Income (Single) | Rate |

|---|---|

| $0 - $48,350 | 0% |

| $48,351 - $533,400 | 15% |

| Over $533,400 | 20% |

| Taxable Income (Married Filing Jointly) | Rate |

|---|---|

| $0 - $96,700 | 0% |

| $96,701 - $600,050 | 15% |

| Over $600,050 | 20% |

The Holding Period Impact

$10,000 gain, 24% income tax bracket:

| Holding Period | Tax Rate | Tax Owed | After-Tax Gain |

|---|---|---|---|

| 11 months | 24% (ordinary) | $2,400 | $7,600 |

| 13 months | 15% (LTCG) | $1,500 | $8,500 |

Difference: $900 saved by waiting 2 more months

The Net Investment Income Tax (NIIT)

Additional 3.8% Tax

High earners pay an additional 3.8% surtax on net investment income.

Threshold:

- Single: MAGI over $200,000

- Married filing jointly: MAGI over $250,000

Applies to: Capital gains, dividends, interest, rental income, passive income

Combined Maximum Rates

For highest earners:

- Long-term capital gains: 20% + 3.8% NIIT = 23.8%

- Short-term capital gains: 37% + 3.8% NIIT = 40.8%

How Different Investments Are Taxed

Stocks and ETFs

Short-term: Ordinary income rates Long-term: Preferential LTCG rates (0%, 15%, 20%)

Mutual Fund Distributions

Even if you don't sell, mutual funds may distribute capital gains annually.

Types:

- Short-term capital gain distributions: Taxed as ordinary income

- Long-term capital gain distributions: Taxed at LTCG rates

Tax-efficient alternative: ETFs or tax-managed funds

Real Estate

Primary residence:

- Exclusion: Up to $250,000 gain (single) or $500,000 (married)

- Must have owned and lived in for 2 of last 5 years

Investment property:

- Subject to capital gains tax

- Depreciation recapture taxed at 25%

- 1031 exchange can defer gains

Collectibles

Items: Art, antiques, coins, stamps, precious metals

Tax rate: Maximum 28% (regardless of holding period)

Cryptocurrency

Treated as property:

- Short-term: Ordinary income rates

- Long-term: LTCG rates

Every trade is taxable: Crypto-to-crypto exchanges trigger gains/losses

Tax-Saving Strategies

Hold for Long-Term

Simple but powerful: Wait at least a year and a day before selling appreciated assets.

The math: 15% vs. 22-37% (depending on bracket) = significant savings

Harvest Tax Losses

Tax-loss harvesting: Sell investments at a loss to offset gains

Example:

- $10,000 long-term gain from Stock A

- $4,000 loss from Stock B

- Net taxable gain: $6,000

Excess losses: Up to $3,000 can offset ordinary income; remainder carries forward

Wash sale rule: Can't repurchase "substantially identical" security within 30 days

Use the 0% Bracket

Strategy: In low-income years, realize gains at 0% rate

Examples:

- Year between jobs

- Early retirement before Social Security

- Graduate school year

How: Sell appreciated investments, immediately repurchase at higher basis

Offset Gains with Losses

Netting rules:

- Short-term gains offset by short-term losses

- Long-term gains offset by long-term losses

- Net short-term and net long-term offset each other

Strategy: Harvest losses to match gains realized

Give to Charity

Donate appreciated assets instead of cash:

- Deduct full fair market value

- Avoid paying capital gains tax

- Must have held over one year

Example: $10,000 stock with $3,000 basis

- Sell and donate cash: Pay ~$1,050 LTCG, donate $10,000

- Donate stock directly: No LTCG, deduct $10,000

Step-Up in Basis at Death

What it means: When you die, heirs receive assets at current market value (stepped-up basis)

Impact: All unrealized gains are never taxed

Strategy: Hold highly appreciated assets until death (for estate planning)

Qualified Opportunity Zones

Defer and reduce capital gains by investing in qualified opportunity zone funds

Benefits:

- Defer gain until 2026 (or sale of QOZ investment)

- Exclude 10% of gain if held 5+ years

- Exclude future gains if held 10+ years

Capital Gains and Retirement Accounts

Tax-Advantaged Accounts

Inside 401(k), IRA, Roth IRA: No capital gains tax on trades

Traditional accounts: Pay ordinary income tax on all withdrawals Roth accounts: Pay nothing on qualified withdrawals

Strategy Implications

Hold high-growth investments in tax-advantaged accounts when possible Hold tax-efficient investments (index funds, stocks you'll hold long-term) in taxable

Reporting Capital Gains

Form 8949

Reports each sale:

- Description of property

- Date acquired

- Date sold

- Proceeds

- Cost basis

- Gain or loss

Schedule D

Summarizes Form 8949:

- Total short-term gains/losses

- Total long-term gains/losses

- Net capital gain or loss

Cost Basis Reporting

Since 2011, brokerages report cost basis to IRS (for covered securities)

Still verify: Ensure reported basis is correct, especially for older holdings

Common Situations

Inherited Investments

Basis: Stepped up to value at date of death Holding period: Automatically long-term

Example:

- Parent bought stock at $10

- Worth $100 at death

- Your basis: $100 (no tax on $90 gain)

Gifted Investments

Basis: Donor's original basis (carryover) Holding period: Includes donor's holding period

Exception: If fair market value is less than donor's basis, special rules apply

Divorce Transfers

Between spouses: Generally tax-free Basis: Carries over from spouse

Home Sale

Exclusion: $250,000 (single), $500,000 (married) Requirements: Owned and lived in for 2 of last 5 years

Planning Throughout the Year

January-November

- Track realized gains and losses

- Identify tax-loss harvesting opportunities

- Consider holding period before selling

December

- Calculate year-to-date gains/losses

- Harvest losses if beneficial

- Realize gains at 0% rate if applicable

- Review mutual fund expected distributions

At Tax Time

- Gather all 1099-B forms

- Verify cost basis accuracy

- Complete Form 8949 and Schedule D

- Consider impact on other taxes (Medicare premiums, etc.)

Taking Action

For Current Investments

- Review holding periods before selling

- Calculate unrealized gains/losses

- Identify tax-loss harvesting opportunities

- Consider which accounts hold which investments

For New Investments

- Buy in tax-appropriate accounts

- Track cost basis from the start

- Plan for long-term holding when possible

Annually

- Review portfolio for harvesting opportunities

- Check mutual fund expected distributions

- Rebalance in tax-efficient manner

- Consider Roth conversions in low-income years

Understanding capital gains tax is essential for investment success. The difference between short-term and long-term rates is substantial—often 10-20 percentage points. By holding investments long-term, harvesting losses strategically, and using tax-advantaged accounts wisely, you can keep more of your investment gains where they belong: in your pocket.

Strategies to Minimize Capital Gains Tax

1. Hold for the Long Term The simplest strategy: hold investments for at least 366 days to qualify for long-term rates.

The difference between 22% (short-term, income bracket) and 15% (long-term) on $50,000 in gains saves $3,500.

2. Use Tax-Loss Harvesting Sell losing investments to offset winning investments.

$20,000 in gains offset by $15,000 in losses means you only pay tax on $5,000. Plus $3,000 of excess losses can offset ordinary income.

3. Donate Appreciated Stock to Charity Instead of selling stock and donating cash, donate the stock directly.

You get a full fair market value deduction AND avoid paying capital gains tax entirely. On $10,000 of appreciated stock with a $3,000 cost basis, this saves $1,050 in capital gains tax plus provides a $2,200 income tax deduction (22% bracket).

4. Use the 0% Capital Gains Bracket In 2026, singles with taxable income under $48,350 pay 0% long-term capital gains tax.

Retirees and gap-year workers can strategically sell investments in low-income years to realize gains tax-free.

5. Step-Up in Basis at Death Inherited investments receive a "step-up" in cost basis to the fair market value at the date of death.

If your parent bought stock at $10 and it is worth $100 when they die, your cost basis is $100—not $10. Selling immediately triggers zero capital gains.

Comments (0)

No comments yet. Be the first to share your thoughts!

Leave a Comment