Social Security is the foundation of retirement income for most Americans, yet few understand how it actually works. How are benefits calculated? When should you claim? How does working affect your benefits? This guide explains everything you need to know about Social Security in 2026 and beyond.

Social Security Benefits: The 2026 Numbers

| Metric | 2026 Amount |

|---|---|

| Maximum benefit (at full retirement age) | ~$4,018/month |

| Average retirement benefit | ~$1,976/month |

| Full retirement age (born 1960+) | 67 |

| Early retirement (age 62) | ~30% reduction in benefits |

| Delayed retirement credit (per year past FRA) | 8% increase |

| Maximum benefit (if delayed to 70) | ~$4,982/month |

| COLA increase (2026) | 2.5% |

| Earnings test (under FRA) | $1 withheld per $2 over $22,320 |

When to Claim: The $100,000+ Decision

| Claim Age | Monthly Benefit (avg earner) | Lifetime Total (to age 85) | Break-Even vs. 62 |

|---|---|---|---|

| 62 | $1,383 | $382,000 | N/A (baseline) |

| 67 (FRA) | $1,976 | $426,000 | Age 80 |

| 70 | $2,450 | $441,000 | Age 82 |

The math: If you live past 82, delaying to 70 pays more total than claiming at 62. Since the average 65-year-old lives to 84-86, delaying is usually the better financial decision—especially for the higher-earning spouse in married couples. ## Social Security Basics

What It Is

Social Security is a federal insurance program providing:

- Retirement benefits

- Disability benefits (SSDI)

- Survivor benefits

- Medicare eligibility

Funded through payroll taxes (FICA): 6.2% from employee, 6.2% from employer.

How You Qualify

Earn credits through work:

- 1 credit per $1,730 of earnings (2026)

- Maximum 4 credits per year

- Need 40 credits (10 years of work) for retirement benefits

2026 Social Security Numbers

- Average retirement benefit: ~$1,900/month

- Maximum benefit at FRA: ~$3,800/month

- COLA increase for 2026: 2.8%

- Maximum taxable earnings: $176,100

How Benefits Are Calculated

Your Average Indexed Monthly Earnings (AIME)

Social Security averages your highest 35 years of earnings, indexed for wage inflation.

What this means:

- Years with no earnings count as $0

- Working fewer than 35 years lowers your average

- Higher earnings = higher benefits (up to the maximum)

The Benefit Formula (PIA)

Your Primary Insurance Amount (PIA)—the base monthly benefit—is calculated using bend points:

2026 bend points (approximate):

- 90% of first ~$1,200 of AIME

- 32% of AIME between ~$1,200 and ~$7,400

- 15% of AIME over ~$7,400

Example: AIME of $6,000

- 90% of $1,200 = $1,080

- 32% of $4,800 = $1,536

- PIA = $2,616/month

Early vs. Late Claiming

Your PIA is your benefit at Full Retirement Age (FRA). Claiming earlier or later adjusts this amount.

Full Retirement Age by birth year:

- 1955: 66 and 2 months

- 1956: 66 and 4 months

- 1957: 66 and 6 months

- 1958: 66 and 8 months

- 1959: 66 and 10 months

- 1960+: 67

When to Claim: The Big Decision

Claiming at 62 (Earliest)

Reduction: ~30% less than FRA benefit (for FRA of 67)

Example: FRA benefit of $2,500

- Age 62 benefit: ~$1,750/month

- Permanent reduction

When it makes sense:

- Health concerns (shorter life expectancy)

- Need income immediately

- Enables earlier retirement

- Spouse with higher benefit who will delay

Claiming at FRA (67 for most)

Benefit: 100% of your PIA

When it makes sense:

- Average life expectancy

- Have other income sources

- Want balance of benefit size and years received

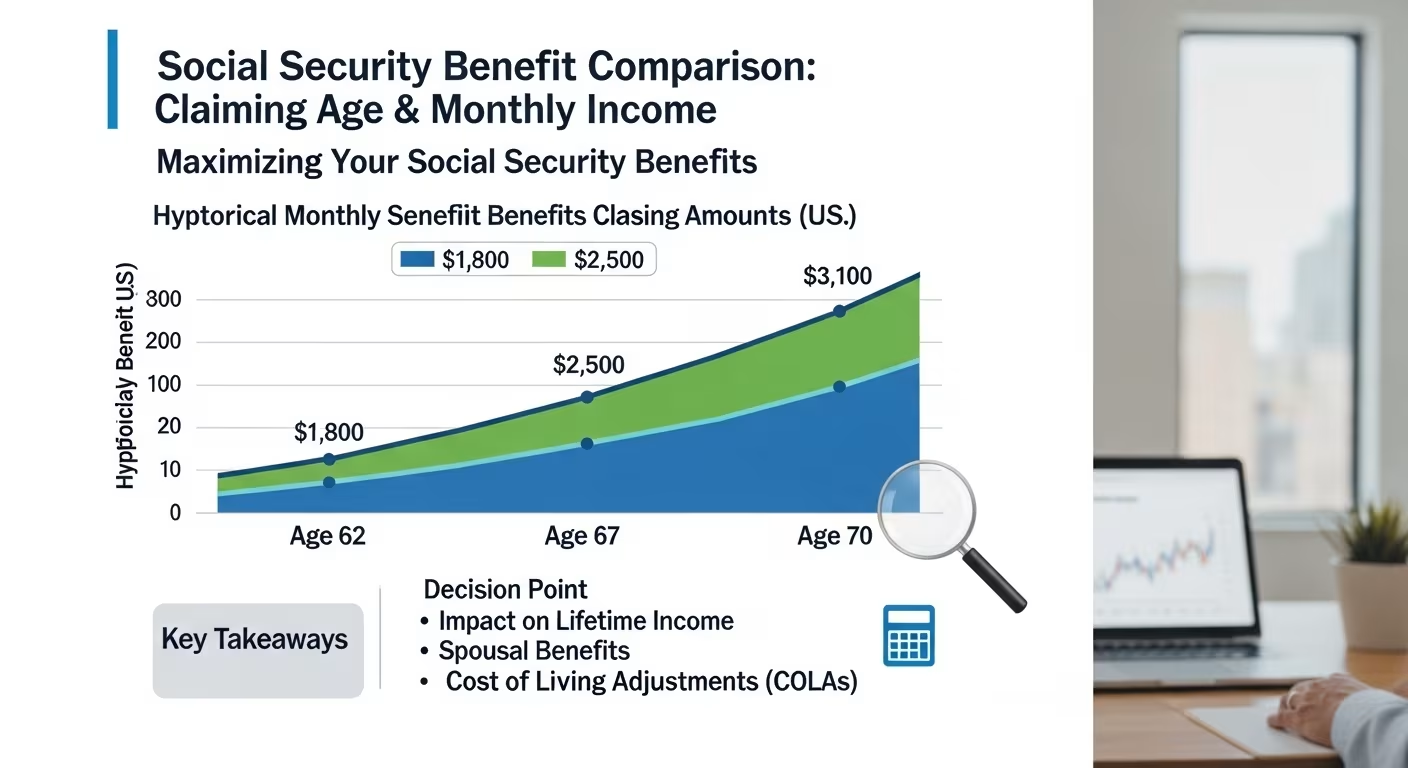

Delaying to 70

Increase: 8% per year beyond FRA (24% more than FRA if delayed from 67 to 70)

Example: FRA benefit of $2,500

- Age 70 benefit: ~$3,100/month

- Permanent increase

When it makes sense:

- Excellent health/longevity

- Still working

- Spouse benefits from your higher benefit

- Want maximum lifetime benefits

Break-Even Analysis

Break-even between 62 and 70: Approximately age 82

- If you live past 82: Delaying typically pays more total

- If you die before 82: Early claiming provides more total

The catch: You don't know when you'll die. Delaying is "longevity insurance."

Spousal Benefits

How They Work

A spouse can claim benefits based on their own work record OR up to 50% of their spouse's PIA—whichever is higher.

Example:

- Your PIA: $2,400

- Spouse's own PIA: $800

- Spouse's spousal benefit: $1,200 (50% of yours)

- Spouse receives: $1,200 (spousal is higher)

Requirements

- Married at least 1 year

- Spouse must have filed for benefits (or be 62+)

- Must be 62+ to claim spousal benefits

Divorced Spouse Benefits

If married 10+ years:

- Can claim on ex-spouse's record

- Ex-spouse doesn't need to have claimed

- Doesn't affect ex-spouse's benefit

- Must be currently unmarried

Survivor Benefits

Widow/Widower Benefits

Surviving spouse can receive:

- 100% of deceased spouse's benefit (at survivor's FRA)

- Reduced benefit starting at 60

- 71.5% at age 60

Strategies for Couples

If one spouse has significantly higher earnings:

- Lower earner claims early

- Higher earner delays to 70

- After higher earner's death, survivor gets the larger benefit

This "claim and switch" maximizes lifetime household benefits.

Working While Receiving Benefits

Before Full Retirement Age

Earnings limit (2026): ~$22,320

If you earn more:

- $1 reduction for every $2 over limit

- Benefits aren't lost—just delayed

Example: Earn $30,000, benefit reduced by $3,840 ($7,680 over limit ÷ 2)

Year You Reach FRA

Higher limit: ~$59,520 (only counts earnings before FRA month) - $1 reduction for every $3 over limit

At and After FRA

No earnings limit: Earn unlimited without benefit reduction

Benefits Aren't "Lost"

Withheld benefits due to earnings are credited back after FRA, slightly increasing your future monthly benefit.

Taxation of Benefits

Are Benefits Taxable?

Depends on "combined income" (adjusted gross income + nontaxable interest + 50% of SS benefits):

Single filers:

- Under $25,000: Benefits not taxed

- $25,000-$34,000: Up to 50% taxable

- Over $34,000: Up to 85% taxable

Married filing jointly:

- Under $32,000: Benefits not taxed

- $32,000-$44,000: Up to 50% taxable

- Over $44,000: Up to 85% taxable

Minimizing Taxes on Benefits

- Manage retirement withdrawals to stay under thresholds

- Use Roth withdrawals (don't count as income)

- Consider state of residence (many states don't tax SS)

Social Security Strategies

For Singles

Primary decision: When to claim

Factors to consider:

- Health and longevity expectations

- Need for income vs. portfolio preservation

- Tax implications

General guidance: If healthy, consider delaying toward 70.

For Married Couples

Coordination matters: Two Social Security decisions, not one

Common strategy:

- Lower earner claims at 62-FRA

- Higher earner delays to 70

- Maximizes survivor benefit

Both high earners: Both may benefit from delaying.

For Divorcees

If you qualify on ex-spouse's record:

- Compare your benefit to 50% of ex's PIA

- Claim whichever is higher

- Can switch strategies at FRA

Common Social Security Mistakes

Claiming Too Early

Most people claim at 62. Most would benefit from waiting longer.

Not Understanding Spousal Strategies

Couples often make independent decisions without considering coordination.

Ignoring Survivor Benefits

The higher earner's decision affects survivor's lifetime income.

Assuming Benefits Will Disappear

Social Security faces funding challenges but is unlikely to disappear. Benefits may be reduced, but planning for $0 is unrealistic.

Not Checking Your Statement

Verify earnings records at ssa.gov. Errors can reduce benefits.

The Future of Social Security

The Funding Challenge

Current projections (as of 2026):

- Trust funds projected to be depleted by ~2033-2035

- After depletion, incoming taxes cover ~75-80% of benefits

- Benefits would be reduced without Congressional action

Likely Solutions

- Increased payroll tax cap

- Gradual benefit reductions

- Higher retirement age

- Some combination

What This Means for Planning

- Don't assume $0 from Social Security

- Don't assume 100% of current projections either

- Consider Social Security as one part of retirement income

- Build other savings to reduce dependence

Checking Your Benefits

Create My Social Security Account

Go to ssa.gov to:

- View estimated benefits

- Check earnings record

- Verify information is correct

- Access benefit statements

What to Review

- All years of earnings recorded

- No missing years

- No incorrect amounts

- Estimated benefits at 62, FRA, and 70

Report Errors

If earnings are missing or wrong, contact SSA with W-2s or tax returns as proof.

Taking Action

In Your 20s-30s

- Create my Social Security account

- Understand basics of how benefits work

- Ensure earnings are being recorded

- Focus on building 35 years of earnings

In Your 40s-50s

- Review benefit estimates

- Factor Social Security into retirement planning

- Begin thinking about claiming strategy

- Coordinate with spouse if applicable

In Your 60s

- Finalize claiming strategy

- Consider working until 70 if possible

- Understand how working affects benefits

- Time claim with other income sources

At Claiming Time

- Apply 3 months before desired start date

- Consider whether to suspend and restart later

- Coordinate with spouse

- Understand Medicare enrollment implications

Social Security is likely your largest retirement asset. Understanding how it works—and making smart claiming decisions—can mean hundreds of thousands of dollars in lifetime benefits. Take time to plan this decision carefully.

Strategies to Maximize Social Security

- Work at least 35 years: Benefits are based on your highest 35 earning years. Fewer than 35 years means zeros are averaged in, reducing your benefit.

- Earn more in peak years: Benefits are calculated on inflation-adjusted earnings. Higher income in your 50s and 60s can replace lower-earning years from your 20s.

- Coordinate with your spouse: The lower-earning spouse can claim early while the higher earner delays to 70, maximizing the survivor benefit.

- Understand the earnings test: If you claim before FRA and continue working, benefits are temporarily reduced ($1 for every $2 earned above $22,320). However, these reductions are credited back after FRA.

- Check your statement: Create an account at ssa.gov to verify your earnings record and projected benefits. Fix errors immediately—they can reduce your benefit permanently.

Social Security and Taxes

Up to 85% of Social Security benefits may be taxable depending on your "combined income" (AGI + non-taxable interest + 50% of Social Security benefits):

| Filing Status | Combined Income | % of Benefits Taxable |

|---|---|---|

| Single | Under $25,000 | 0% |

| Single | $25,000-34,000 | Up to 50% |

| Single | Over $34,000 | Up to 85% |

| Married | Under $32,000 | 0% |

| Married | $32,000-44,000 | Up to 50% |

| Married | Over $44,000 | Up to 85% |

Comments (0)

No comments yet. Be the first to share your thoughts!

Leave a Comment