Pay Off Debt or Save First? Here's How to Decide

The question of whether to pay off debt or save first doesn't have a single universal answer — and advice that pretends otherwise is ignoring your actual financial situation. The right choice depends on the type of debt you carry, the interest rate attached to it, what savings you're trying to build, and several other factors that vary from person to person. This article gives you a decision framework for your specific circumstances rather than a generic rule that may cost you real money.

Why the Pay Off Debt or Save Decision Actually Matters

When you decide to pay off debt or save your extra cash, you're making a decision about the return on your money. Every dollar directed toward high-interest debt earns a guaranteed return equal to the interest rate you're no longer paying. Every dollar saved earns a return based on the interest rate or investment return on that savings vehicle. Getting this allocation right can make a material difference in your long-term financial position.

Directing all available cash toward debt repayment when you have no savings leaves you financially fragile — one car repair or medical bill away from adding more debt. Directing all available cash toward savings when you're paying 24% APR on a credit card means you're earning 4-5% on savings while losing 24% on debt — a net loss of nearly 20 cents on every dollar per year. Neither extreme is optimal for most people. The right answer lives somewhere in between, calibrated to your specific numbers.

The framework below helps you think through the tradeoffs systematically rather than by gut feeling alone.

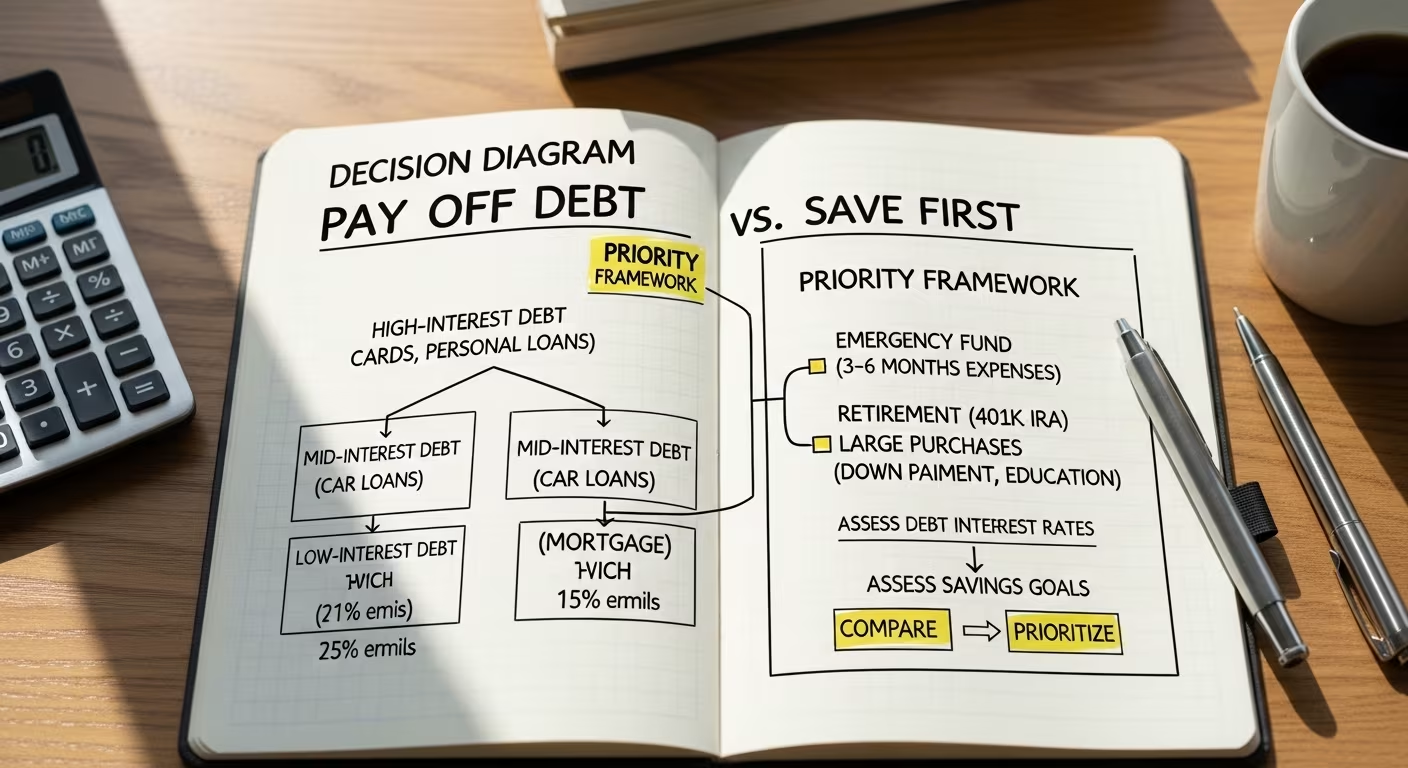

Step One: Identify Your Debt Types and Interest Rates

Not all debt is equal. The first task is to list every debt you carry, its current balance, and its interest rate. This typically reveals a spectrum from beneficial or neutral debt to genuinely costly debt.

Low-rate debt (under 6-7%). Mortgages, some student loans, and auto loans taken at favorable rates often fall in this range. This debt is relatively cheap. Mathematically, money directed toward investing — where long-term average stock market returns have historically been 7-10% annually — may produce better outcomes than aggressively prepaying this debt.

Mid-range debt (7-12%). Some student loans, personal loans, and older auto loans fall here. The math gets closer. Whether to prioritize payoff versus investing depends on your specific numbers and your risk tolerance around carrying debt.

High-interest debt (above 12%). Credit card debt typically falls here, often at 20-27% APR. Carrying-charge plans, payday loans, and some personal loans can be even higher. Paying off this debt offers a guaranteed return equal to the interest rate — a return almost no investment can reliably beat. For high-interest debt, aggressive payoff is almost always the mathematically correct choice.

Step Two: Build a Minimum Emergency Fund First

Before tackling debt beyond minimums or investing beyond employer match, most financial planners recommend establishing a basic emergency fund — typically $1,000 to $2,000 for people actively paying down high-interest debt.

Here's why: without any savings buffer, a single unexpected expense almost guarantees new debt. You pay down your credit card, then your water heater fails, and you're right back where you started — or worse. The emergency fund is the circuit breaker that prevents this cycle from perpetuating indefinitely.

A minimal emergency fund isn't the full three-to-six month version. It's just enough to handle the most common financial curveballs without reaching for a credit card. Once high-interest debt is eliminated, you can build this out to a full emergency fund.

Step Three: Capture Any Employer 401(k) Match

If your employer offers a retirement contribution match and you're not contributing enough to capture it, that's the first place to direct available dollars before tackling debt. An employer match is a guaranteed 50-100% return on your contribution — no investment can compete with that, even when weighed against high-interest debt payoff.

Example: your employer matches 100% of contributions up to 4% of your salary. If you earn $60,000 and contribute 4%, you put in $2,400 — and your employer adds another $2,400. That's an instant 100% return on those dollars before any investment growth occurs. Walking away from that match is leaving free money behind permanently.

After capturing the full employer match, refocus on high-interest debt elimination.

Step Four: Apply the Interest Rate Decision Rule

Once you have your basic emergency fund in place and you're capturing any employer match, the core decision rule is straightforward: compare your debt's interest rate to your expected after-tax investment return.

If the debt interest rate is higher than what you'd reasonably expect to earn after taxes on invested money, pay off the debt first. If the debt interest rate is lower, investing may produce better long-term outcomes.

A common threshold is 6-7%. Debt above this threshold typically warrants aggressive payoff. Debt below this threshold can reasonably be paid on schedule while you invest the difference.

This isn't a guarantee — investment returns are variable and debt payoff returns are guaranteed. Risk tolerance matters here. Some people correctly observe that they'd sleep better carrying no debt even at low rates, and the psychological benefit has real value. Others are comfortable carrying low-rate debt to maintain higher investment contributions. Both approaches can be rational depending on your situation and temperament.

The Avalanche vs. Snowball Debate

Two popular debt payoff strategies deserve mention when discussing how to pay off debt efficiently:

The debt avalanche directs extra payments toward the highest-interest debt first while making minimums on everything else. This is mathematically optimal — it minimizes total interest paid and eliminates debt fastest in terms of total dollars out of pocket.

The debt snowball directs extra payments toward the smallest balance first, regardless of interest rate. Popularized by Dave Ramsey, this approach produces psychological wins early in the process — paying off an account entirely motivates continued behavior. For people who've struggled with follow-through, the behavioral boost of the snowball can produce better real-world results even if the math is slightly worse.

Either approach is dramatically better than making minimums without directing extra cash purposefully. Choose the method that matches your psychology and that you'll actually stick with over months or years.

What About Saving for Specific Goals?

The pay off debt or save question gets more nuanced when you're saving for something specific — a home down payment, a car to replace one that's failing, a planned medical expense.

If the goal is time-sensitive and necessary, you may need to save for it simultaneously with debt payoff rather than waiting until debt is gone. A practical approach: calculate a minimum monthly amount you need to save to reach the goal in the required timeframe, and direct the rest of available cash toward debt. This isn't mathematically optimal, but it's often practically necessary given real-world constraints.

For goals that aren't time-sensitive, delaying them until high-interest debt is eliminated usually makes financial sense. Every month you carry high-interest debt while building a savings account earning 4-5% is a net monthly loss that compounds against you.

Common Mistakes People Make With This Decision

Ignoring the math entirely. Some people pay off every debt as fast as possible regardless of interest rate, including 3% mortgages, while earning 5-7% on investments. This is emotionally satisfying but can cost meaningful money over long time horizons.

Ignoring the psychology entirely. Other people make the spreadsheet-optimal decision while hating the feeling of carrying debt, which causes stress that undermines other financial behaviors. Your optimal solution has to be one you'll actually follow through on consistently.

No emergency fund before attacking debt. This leads to the yo-yo pattern — pay down debt, unexpected expense hits, add debt back. The $1,000-$2,000 buffer breaks this cycle decisively.

Skipping the employer match. Leaving employer match money on the table is almost always a financial mistake, even when carrying debt. The math rarely works out in favor of skipping it.

Confusing minimum payments with real progress. On high-interest revolving debt, minimum payments may cover little or no principal. You can make minimum payments for years while the balance barely moves. This isn't a debt payoff strategy — it's treading water at significant cost.

Building Your Decision in Practice

Here's how to put this framework into action with a concrete sequence:

- List all debts with current balance and interest rate

- If no emergency fund exists: direct cash toward a $1,000-$2,000 buffer first

- If employer match isn't fully captured: contribute enough to get the full match

- For debts above roughly 7% APR: pay aggressively, starting with highest-rate debt (avalanche) or smallest balance (snowball)

- For debts below roughly 7% APR: pay on schedule, direct remaining available cash toward investments

- Once high-interest debt is gone: build emergency fund to full three to six months of expenses

- Increase retirement and investment contributions systematically

This sequence isn't rigid — life is messier than frameworks. But having a clear sequence means your money decisions have a logic to them rather than being driven by whichever financial priority feels most urgent in a given week.

The Consumer Financial Protection Bureau offers free tools for modeling debt payoff scenarios at consumerfinance.gov.

Using a Spreadsheet to Run Your Own Numbers

The best way to make this decision well is to model your specific numbers. Build a simple spreadsheet with your debts, their rates, your monthly cash flow available for financial goals, and two scenarios: one where you prioritize debt, one where you split between debt and savings.

Calculate the total interest you'd pay in each scenario and the projected savings or investment value at the end of the same period. The difference is concrete and often illuminating. Many people are surprised by how significant the gap is when they actually run the numbers — in either direction.

Revisit the Decision Regularly

Your financial situation changes. Income increases, debt gets paid down, interest rates shift. The allocation that made sense when you had $15,000 in credit card debt may not make sense once that debt is down to $3,000. Build a habit of revisiting your debt-vs-savings strategy at least annually, or whenever a significant financial change occurs.

The goal isn't to find the one perfect answer and lock it in forever — it's to keep making increasingly informed decisions as your financial picture evolves. Small improvements in allocation today compound into significant wealth differences over a decade.

Managing the Emotional Side of Debt Payoff

The decision to pay off debt or save isn't purely mathematical — it has an emotional dimension that's worth acknowledging. Carrying debt, particularly high-interest consumer debt, often produces a persistent background stress that affects your quality of life beyond the financial numbers. Some people find that this stress impairs their decision-making in other areas of life, making the psychological case for aggressive debt payoff stronger than the spreadsheet alone would suggest.

On the other side, people who've never had any savings often feel a level of financial anxiety that aggressive debt payoff without any buffer doesn't fully address. Building even a small savings cushion can reduce that anxiety enough to make the overall system work better in practice.

The most sustainable approach respects both the math and the psychology. If carrying debt is genuinely distressing, weight your strategy toward faster payoff even if it's not technically optimal. If building savings produces a sense of security that helps you stay employed, stay healthy, and make better decisions, that benefit has real financial value that doesn't show up in an interest rate calculation.

Pay attention to how different approaches feel as you experiment with them. The best financial strategy is almost always the one you'll actually follow through on consistently over the months and years it takes to see meaningful results.

None of this is financial advice. Your situation depends on variables this article can't see — taxes, risk tolerance, time horizon, dependents. A fiduciary advisor can model your specific case.

Comments (0)

No comments yet. Be the first to share your thoughts!

Leave a Comment