If you have wished your portfolio would just get away from you without having to touch the controls all the time, then, DRIPs (Dividend Reinvestment Plans) are a simple way to do so. A Dividend reinvestment plan (DRIP) buys shares from dividend payments automatically, opting out of cash dividends at the request of the investor. This allows the investor to purchase shares (including fraction shares) of the stock or ETF in question. That small automation will keep compounding every quarter (or month) while you’re busy doing other things.

This guide explains how dividend reinvestment works, the difference between broker DRIPs and company/transfer agent DRIPs, tax realities in taxable vs retirement accounts, when to turn off DRIP (yes, sometimes you should), and a practical, copy-paste setup so you can set-and-forget your investing (without becoming set-and-ignore).

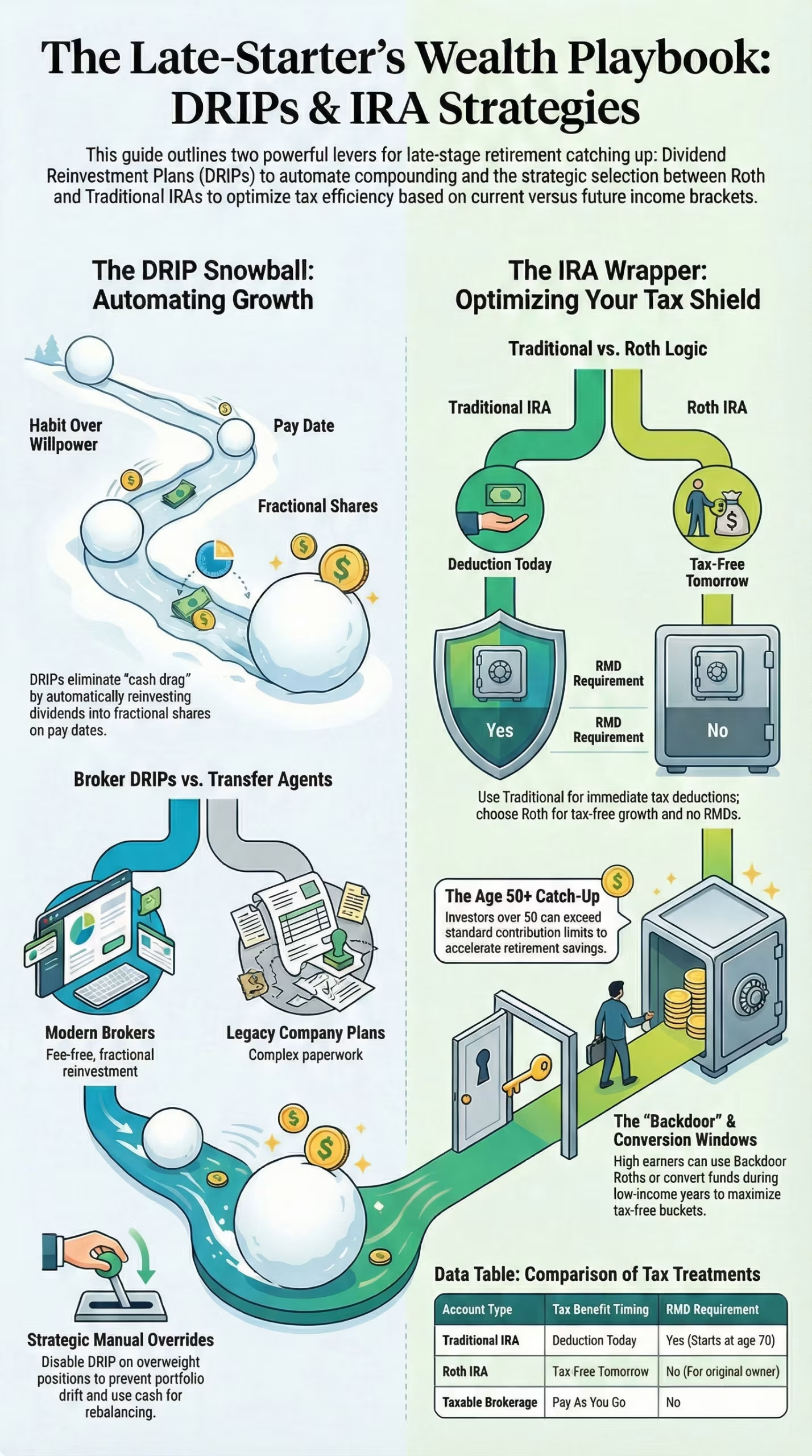

What Is a DRIP and How Does it Work? 🧩

A Dividend Reinvestment Plan automatically buys more shares of a holding that pays dividends using the cash dividends that investment generates on the pay date. Most of the new age brokers support fractional shares. Therefore, even small dividends will buy tiny pieces of a stock or ETF units that will thus earn the next dividend, and so forth. That’s compounding by habit, not by willpower.

Eliminating cash drag is important so missed reinvestments do not occur. This investment reinforces a long-term dollar cost averaging appeal inside one single ticker.

Two Paths — Broker DRIPs and Company/Transfer-Agent DRIPs

Broker DRIP (the Common Default)

- You hold shares at a mainstream brokerage.

- You toggle “Reinvest dividends” per position.

- Reinvestments are typically fee-free and fractional.

- Automatic recordkeeping (cost basis tracks every little lot).

Company/Transfer-Agent DRIP (Legacy/Direct)

- You sign up with the company’s transfer agent (e.g., via a DSPP/DRIP).

- At times, offers opportunities to buy cash and discount on reinvestment.

- Might impose minor service fees, restrict fractional handling, and make ACATS transfers complex.

- Admin mailers, separate tax docs, and slower UX.

Most investors today find a broker DRIP cleaner, cheaper, and easier. A transfer-agent DRIP is only worth considering if the issuer offers a true reinvestment discount that outweighs the fees and the hassle.

Pros and Cons (So You’re Not Surprised) ⚖️

Pros

- Automatic compounding lets every dividend be working capital.

- Promotes confidence and decisiveness among prospects.

- Fractional power makes small payouts useful and smoothes timing risk.

- Hands-off alignment is great for “buy, hold, rebalance” strategies.

Cons

- The dividends can be reinvested but still tax is required to be paid in that year.

- One way to nudge an allocation off-target over time is through DRIP.

- Many investors have a blind spot when it comes valuing opportunities. Your reinvestment (dividends, new money, etc.) goes into whatever is today’s price. That’s great for habit but not great for valuation timing.

- Extra to-do’s (admin clutter, company DRIPs): fees, paperwork, odd-lot positions.

DRIPs in Taxable vs Retirement Accounts 🧾

Taxable Brokerage

- Dividends that are qualified may have reduced rates, while non-qualified dividends are taxed at the standard individual income tax rate like regular income.

- When you reinvest your dividends, they increase your cost basis.

- Hang on to your 1099-DIV, and have your broker track lots; also download a tax-lot report each year.

IRA/401(k)/Roth

- Most dividends aren’t taxable at the moment; DRIP is usually a no-brainer.

- A Roth IRA allows your reinvested dividend to grow tax-free if rules are followed.

- In a Traditional IRA/401(k) taxes are deferred to withdrawal time which is still okay to DRIP.

It’s often best to use DRIP for retirement accounts as it’s easy and clean. Even in taxable, it’s still solid—just remember taxes and rebalancing.

When to Turn DRIP Off and Take Cash

- You need cash flow (retirees drawing income).

- You are rebalancing; you want dividends to build a bond or underweighted sleeve.

- Valuation discipline: redeploy dividends into underweighted holdings.

- Tax planning: in a high bracket, let dividends pool in cash/money market to offset gains elsewhere.

Because DRIP is per-holding, you can keep it on for broad ETFs yet take cash from an overvalued single stock.

What to DRIP (and What to Leave Alone) 🎯

Great DRIP Candidates

- Broad ETFs (total market, S&P 500, dividend growth ETFs).

- Dividend payers with sensible payout ratios, steady cash flow, and strong balance sheets.

- REIT ETFs in retirement accounts (to shield ordinary-income dividends).

Maybe Don’t DRIP

- High-yield traps (unsustainable payouts, rising debt).

- Positions already overweight in your portfolio.

- Stocks you plan to trim soon.

Quick filter: ten-year dividend growth, reasonable payout ratio, stable margins, controlled leverage. Aim for “boring” excellence.

The Mathematics of DRIP: A Quiet but Powerful Compounder

Consider a $10,000 position yielding 3%, paid quarterly. With dividends reinvested and a modest price-growth assumption, your share count increases every quarter. If the price trades sideways for one year, you get a bigger income next year because you own more shares. That’s the snowball. Ongoing contributions (even small) let DRIP act like dollar-cost averaging inside a single ticker.

Do this one time only:

- Select a DRIP list (broad ETFs + any dividend growers to hold 5–10+ years).

- Toggle “Reinvest dividends” per holding at your broker.

- Auto-contribute each payday (even $50–$200 helps).

- Calendar two reviews per year.

- Midyear: check allocation drift; disable DRIP on any sleeve that’s too large.

- Year-end: export tax lots for taxable; confirm cost basis and fees.

- Name your goal (e.g., “Dividends → future trips / early-retirement buffer”).

Fees, Minimums, and Fractional Shares 💵

Most broker DRIPs are free and support fractional shares. Transfer-agent DRIPs may charge per reinvestment or optional cash purchases; always check the fee table. DSPPs often require small minimums—brokers are usually easier.

Common Mistakes (and Easy Fixes) 🧯

- Letting one stock hit 20%+ of the portfolio. Fix: turn off DRIP there; redeploy dividends into diversified ETFs.

- Ignoring taxes in taxable accounts. Fix: expect a 1099-DIV; keep some cash to cover April if needed.

- Chasing the highest yield. Fix: prioritize quality and dividend growth, not headline yield.

- Never reviewing allocations. Fix: two check-ins per year; automation should serve your plan.

Tips, Tricks, Hacks & Local Secrets 💡

- DRIP the ETFs; take single-stock dividends in cash to keep flexibility.

- Use a Roth IRA to reinvest the highest-yield sleeves tax-free.

- Round odd fractional lots with tiny scheduled buys if you care about whole-share aesthetics.

- Keep an ex-date/pay-date calendar to anticipate cash flows.

- Turn off DRIP on overweight funds; route those dividends to underweight assets for “no-sell” rebalancing.

- Log dividend raises for motivation; automation should serve your thesis—pause if a company cuts.

Mini Case Studies (Copy the Playbook) 📚

The Busy Professional (Age 40, Roth & Taxable)

- Roth: DRIP a total-market ETF and a dividend-growth ETF.

- Taxable: DRIP only the broad ETF; take single-stock dividends in cash for rebalancing.

- Two reviews per year; no trading between.

The Late Starter (Age 52, Catch-Up Mode)

- Auto-contribute each payday to a dividend-growth ETF in the 401(k).

- In taxable, stop DRIP to shift dividends into an underweight international sleeve.

- Goal: smooth compounding while controlling drift.

The Near-Retiree (Income Prep)

- Two years pre-withdrawal: turn off DRIP on at least one equity sleeve; let dividends pool in cash for income needs.

- Keep DRIP on a core dividend-growth ETF in a Roth for tax-free reinvestment even in retirement.

FAQs — DRIPs (Dividend Reinvestment Plans) ❓

What’s a DRIP in investing and how does dividend reinvestment actually work?

Are dividend reinvestment plans right for buyers matching the description?

Are taxes paid on dividends from DRIP accounts in a taxable account if automatically reinvested?

Is it better to use DRIP in a Roth IRA or Traditional IRA than a brokerage?

What differentiates a broker DRIP from a company/transfer-agent DRIP?

Should I reinvest dividends on mutual funds or individual dividend stocks?

When should I turn off DRIP and take dividends in cash?

Do DRIPs buy on the ex-dividend date or the pay date?

Can I use DRIP for ETFs and still abide by my asset allocation?

Do DRIPs work with fractional shares at all brokers?

Are there fees for DRIPs?

Do I have to track cost basis on reinvested dividends?

Is a high dividend yield always better for a DRIP strategy?

Can I pause DRIP temporarily and resume later?

Does DRIP timing matter for volatility?

How do I enable DRIP at my broker?

Is dollar-cost averaging compatible with DRIP?

What about REITs and high-income ETFs—should I DRIP those?

If a company cuts its dividend, will DRIP still buy more?

Can DRIPs help late starters catch up for retirement?

Final Thoughts 💬

DRIPs are great because they automate solid investing behavior. Reinvest where it fits the plan, review allocations twice a year, and then get on with your life while compounding does the heavy lifting. “Set-and-forget” doesn’t mean set-and-ignore—it means your system keeps growing, even when you’re busy.

Comments (0)

No comments yet. Be the first to share your thoughts!

Leave a Comment